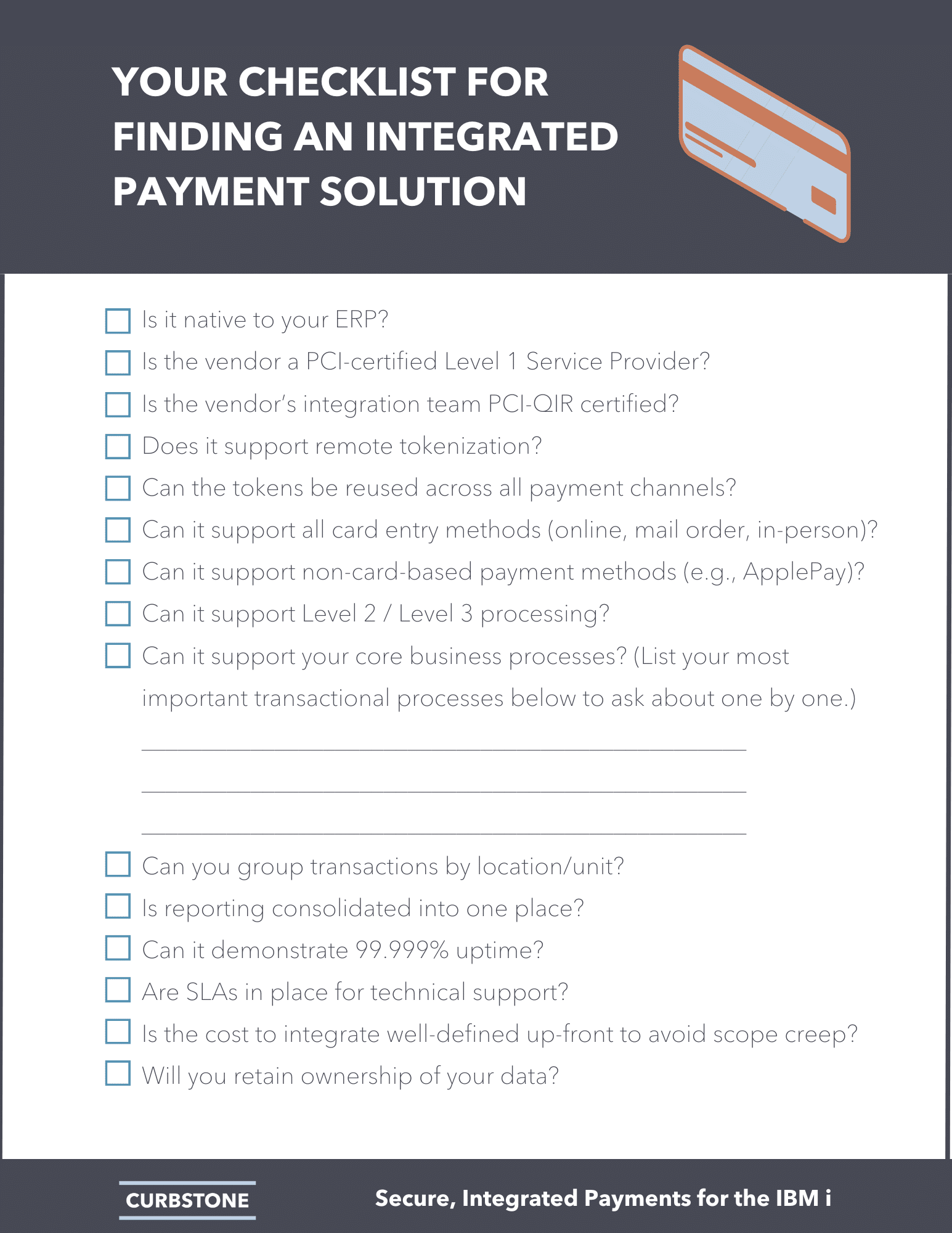

As companies look for ways to increase efficiency across all of their departments – from sales and accounting to operations and production – integrated payments are quickly becoming a business requirement. They don’t just deliver a fast and simple checkout process for customers; they tie transaction data back to other essential business systems, such as an order entry application or an ERP. This gets rid of the data silos that slow down reporting and reconciliation – even for merchants that use several different technologies across multiple sales channels.

1A: Native Integration with Your Existing Business Systems

This is – without a doubt – the gold standard of integrated payments. Solutions that integrate with your ERP, CRM, or financial systems considerably streamline your day-to-day workflows. As you begin your search for an integrated payment platform, check with your existing vendors to see what options are already embedded into their product suite.

1B: Compatibility with Your Existing Business Systems

In a 2021 survey, only four percent of software vendors already offered integrated credit card processing to their customers. 83 percent were planning to develop this feature in the next five years, but there are still many commercial software packages without an integrated payments offering. If your vendors don’t support integrated payments, your business may have to lead the charge – but integrated payment technologies that use the same back-end language as your existing software can make the process much less resource-intensive.

Curbstone, for instance, offers RPG-native payment processing technologies that can seamlessly communicate with any application that runs on the IBM i. Whether that’s a commercial ERP system (like Mincron or Iptor) or a custom order entry application that you built in-house, native compatibility makes the integration process easier on your developers.

The same goes for working source code. If you’re not writing your credit card integration from scratch – and if you have test utilities that you can use throughout the process – you’ll be able to get started more quickly. With Curbstone, some customers have completed their payment integration in a matter of weeks; here’s a look at what’s required behind the scenes.

2: Strong Security Measures that Support PCI Compliance

Integrated or not, any credit card processing platform that you use must be PCI-compliant. Choosing technologies from a PCI-validated Level 1 Service provider help you reduce the amount of reporting your own team needs to do to prove your compliance; this can be the difference between a 22-question SAQ-A and a 300+ question SAQ-D.

That said, there are many ways for an integrated credit card processing system to meet PCI requirements. Each platform may include slightly different security measures. Consider which of the following are must-haves for your business, then ask about each one in your discovery calls with prospective vendors.

It’s increasingly rare for merchants to do business on only one channel – which means it’s important to find an integrated payment solution that can bring together e-commerce sales, mail orders and phone orders, and in-person/EMV transactions. Even if you don’t need all these options right now, it’s a good idea to give yourself the flexibility in a solution to add additional options in the future as your business grows.

If you take payments face-to-face, don’t overlook the hardware aspect. An integrated terminal solution allows you to pass transaction data directly from your credit card terminal to your other systems of record. Not all terminals and point of sale systems support integrated card payments, so it’s worth considering while choosing an integration partner.

4: Support for Your Existing Workflows

There’s nothing worse than spending time and resources on a payment integration, only to find out after it’s done that you can’t process transactions the way you want. (For example, if you can’t process zero-dollar authorizations or issue partial refunds, you’re going to end up with frustrated end users.)

That’s why – when it comes to finding integrated payment platforms for truly seamless transactions – you find one that’s flexible enough to support any back-office workflow. And if those workflows change as your business evolves? Your solution needs to be able to adapt over time as well.

5: “5 Nines” Availability

You need to trust that your integrated payments software won’t go down at inopportune times (of course…is there ever really an opportune time for your credit card system to stop working?) “Five-nines” availability – that is, 99.999% uptime – provides crucial assurance that you’ll be able to accept credit card payments whenever your customers are looking to buy.

In the event that something does go wrong, you’ll want to have a documented SLA (service level agreement) in place with your vendor. A provider that can guarantee a callback in an hour or less can help you quickly troubleshoot any issues that do arise. Additionally: because there are so many components that have to work together in any payment processing infrastructure – from your hardware to your internet service provider to your authorization network and your bank – having a partner who can serve as a liaison with each of these individual entities can speed up the resolution process if something does go wrong.

With Curbstone, secure and efficient integrated payment processing is within reach. We’ve helped hundreds of companies embed credit card processing functionality within their IBM i-based applications – and we’d be happy to do the same for you. To learn more about our integrated payment systems, contact us today.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.